Financial Education for Young Adults: Needed Now More Than Ever Before!

Why it's more important now for young adults to have a financial education and what they can do about it

Hey, you made it here! Congratulations! Welcome to my first blog post. I say "my" first blog post rather than "our" or "NextGen Financial Freedom" because, technically, I am NextGen Financial Freedom. I guess you can call me a solopreneur (I just learned that word a few days ago). Who am I? Good question! You can learn more about me and my background here from the About link on the website. I'm not sure if any of you have ever written a blog before, but there was a lot of pressure in trying to figure out what to write about in my first blog post. What should the topic be? Who am I writing to? What type of tone should I use? Should I be more professional or casual? Who is even going to read this anyway??? Like I said, it's a lot of pressure.

I settled on writing about this topic: "Financial Education for Young Adults: Needed Now More Than Ever Before!". Why? Because that's the whole darn reason why I started this side hustle business, NextGen Financial Freedom (Slogan: Free to live your dreams...pretty catchy, huh!). I do believe in my heart that young adults need to know more about managing their money in today's world than in previous generations. Let me explain why and what you can do about improving your financial education. Hopefully, by following this blog and using some of NextGen Financial Freedom's services, I can help you live a more intentional and meaningful life.

WHY FINANCIAL EDUCATION IS MORE IMPORTANT NOW

I'm not sure if you've ever heard of this metaphor (I forgot where I first heard of it), but it has been said that retirement is a three-legged stool:

a) Your savings

b) Your pension

c) Social Security

Perhaps your grandfather could've relied on each of those three legs to support him in retirement. However, most workers no longer receive an employer pension as they have been replaced by 401k-type plans. So that leg is no longer there for many of you. Your father most likely can rely on two of the remaining legs (personal savings and Social Security), but what about you? What will social security look like by the time you are older? According to this article by GoBankingRates.com, those of you who are a part of Gen Z might have your social security benefits cut, and the age at which you receive benefits raised to 70 years old. This article from MarketWatch mentions that 74% of Americans are not counting on Social Security benefits when counting on retirement income. That leaves you with only one sturdy leg (your savings) and one wobbly leg (Social Security) to count on for your retirement income.

Ok, I get it! You are only in your 20's or 30's and have more immediate, pressing financial needs today besides retirement. You might have questions like: How can I earn a higher income? How can I stop living paycheck-to-paycheck when prices keep going up? Should I pay off my student loan debt or invest in my employer's 401k? How much can I truly afford for big-ticket items like a car and housing? These are all good questions and questions your generation is struggling with more than previous generations. Consider this:

Mortgage rates recently have been at the highest level in over a decade

The median sales price of a home in the United States ($436,800) has more than doubled in the past 10 years

17% of people with a new car or truck are paying more than $1,000 on their monthly car payment

73% of millennials are living paycheck-to-paycheck

With the rise of technology and the increasing accessibility of financial products and services, you are faced with a ton of financial decisions that can have long-term consequences. This isn't your grandfather's or father's economic world you are living in. Knowing how to manage your money at an early age is more critical now than ever before.

WE DIDN'T PREPARE YOU WELL ENOUGH...THAT'S ON US!

The Financial Literacy Crisis in America 2023 report by Ramsey Education shows how bad we are as a country in preparing you to make personal financial decisions. The statistic that sticks out to me from this report is, "72% of U.S. adults said they would be further ahead with their money today if they had a personal finance class in high school". Unfortunately, the report also states that only 17% of those surveyed took a personal finance class in high school. For the educational leaders in this country...that's on us!! As someone I was talking to the other day said, "We live in a capitalist society. It's crazy that we don't make financial education mandatory."

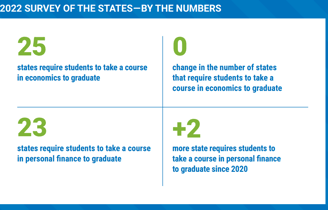

According to the Council For Economic Education's 2022 Survey of the States, only 23 states require high school students to take a personal finance course to graduate. I live in Wisconsin, and we do not require personal finance as a graduation requirement (shame on us!). Research shows that requiring such a course can make a difference in your life. According to this article from the Milwaukee Journal Sentinel, "One study found that among first-generation or low-income students who had taken such a course, loan repayment was higher, which suggests those students were more likely to have finished college and found a higher-paying job."

Take me as an example. I always had an interest in personal finance, but my high school did not offer such a course. It did offer classes like Accounting and Introduction to Business, but not a course on how to handle the day-to-day financial decisions I would need to make as an adult. In college, I majored in Accounting, but I was never required (or recommended) to take a course in personal finance. Rather, all of my courses were geared toward how to handle money for a business. I had to learn about money management from my own interest in reading books on the topic after I graduated.

So if you did not learn about personal finance in school, where does that leave you? Well, you might have been taught some lessons from your parents. But where did they learn how to manage their money? Don't get me wrong. Maybe they talked to you about money often and taught you some valuable lessons. However, according to this article from CNBC, 31% of parents NEVER talk to their children about money. If a) you didn't learn it in school and b) you didn't learn it from your parents (or your parents' money advice was not the best), where does this leave you? I guess "trial and error" or "live and learn" for many of you. For others, perhaps you have taken control of pursuing your own financial education by reading books/websites and asking others who are knowledgeable about investing, budgeting, saving, etc. Maybe that's how you stumbled across this blog post (I'm glad you did!).

YOUR FINANCIAL EDUCATIONAL JOURNEY STARTS TODAY...THAT'S ON YOU!

It's time to take control! No more excuses and blaming others for your financial education. Starting TODAY, it's up to you to learn how to effectively manage your own money and improve your financial wellness. Financial education is not something to run away from; it's a game-changer that can help you achieve your dreams and goals. Imagine having a year's worth of savings built up. Imagine finding your dream job. Imagine being debt-free. Imagine having your retirement funds grow to a point where you can become "work optional" well before most people retire in their mid-60s. Starting TODAY, your financial education journey...that's on you!!

I encourage you to use NextGen Financial Freedom to help. Keep reading this blog. Use any of our services. Encourage your HR department to have NextGen Financial Freedom host a financial wellness workshop for you and your coworkers. Contact NextGen Financial Freedom regarding any questions you have about our services. Read other personal finance blogs and books. Take those baby steps to help achieve your rich life of tomorrow.

Ready, set, GO!!