Lighting Your Wealth on Fire: The Real Cost of Investment Fees

Three college mascots. One investing lesson that could save you hundreds of thousands.

Brett Killion

4/7/20254 min read

Want to know one of the biggest threats to your retirement savings?

It’s not market crashes, poor stock picks, or bad luck.

It’s something so subtle, it often flies completely under the radar…Investment fees.

Yep. Those tiny percentages that seem harmless—expense ratios, sales loads, asset management fees—can quietly steal away hundreds of thousands of dollars from your future self.

Let’s dig into how investment fees—even small ones—can quietly rob you of hundreds of thousands of dollars over time. Yes, seriously. Hundreds of thousands!!

First, a Quick Crash Course on Investment Fees 💸

Before we jump into the numbers, let’s break down the three most common types of investment fees you might run into:

Expense Ratio – This is what the mutual fund company charges to manage the fund. It’s taken automatically every year as a percentage of your invested balance. Think of it like an annual “membership fee,” even if you don’t realize you're paying it.

Asset Under Management (AUM) Fee – If you work with a financial advisor, some charge an annual fee based on how much money they manage for you. For example, 1% of your portfolio per year. Again—automatically deducted, and it grows as your account grows.

Front-End Load – This is a sales commission charged upfront when you buy into a fund. If the front-end load is 5%, and you invest $100, only $95 actually gets invested. The other $5? That’s gone on day one.

These fees may sound small, but over decades, they compound just like your investment returns—except it’s not compounding for you… it’s compounding for someone else.

Let’s Meet Our Investors

To illustrate just how big a deal fees can be, let’s check in with three “investors.” Since I’m a proud University of Wisconsin-Madison grad, we’ll name these investors after a few familiar Big Ten mascots...

Each one starts investing at 25 and contributes:

$1,000 upfront

$500/month until age 65

Their investment earns 8% annually (before fees)

But here's the twist—each one chooses a different mutual fund and financial advisor.

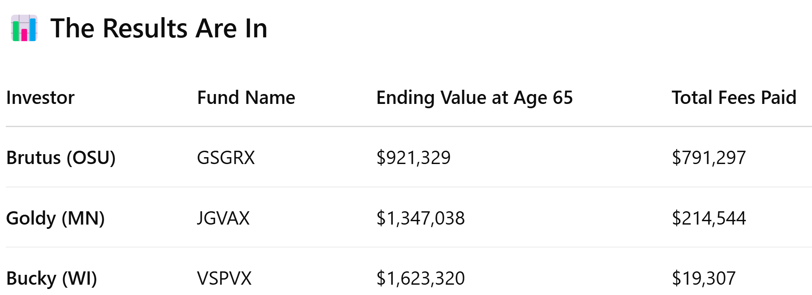

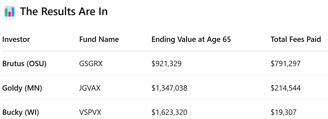

🅾️ Brutus the Buckeye (Ohio State)

Brutus invests in the Goldman Sachs Equity Income Fund (GSGRX). This fund has an expense ratio of 1.00%. Brutus selects Buckeye Wealth Management for his financial advisor which charges Brutus a 1% AUM fee. That's how Buckeye Wealth Management gets paid by Brutus.

🟡 Goldy the Gopher (Minnesota)

Goldy invests in the JPMorgan Growth Advantage Fund (JGVVX). It has a 0.5% expense ratio. Goldy selects Gopher Financial for his advisor. Gopher Financial charges a 5% front-end load every time he adds new money...that's how Gopher Financial gets paid by Goldy.

❤️ Bucky Badger (Wisconsin)

Bucky? He goes the low-cost DIY route. He invests in the Vanguard 500 Index Fund (VSPVX), which has an ultra-low 0.04% expense ratio and no other fees. Since Bucky is a DIY investor, he does not pay any fees for a financial advisor.

All three make the same monthly contribution ($500/month). But look at what happens when they turn 65...

👉 Yes… you’re reading that right. Bucky ends up with nearly $700,000 more than Brutus—despite investing the exact same amount of money.

Where did Brutus’s money go?

Well, over those 40 years, he paid:

$254,684 in direct fees (expense ratio + advisor fee)

$466,613 in opportunity cost—the lost growth he could have earned if those fees had stayed invested

So, What’s the Takeaway?

The cost of investing matters a lot. You don’t always see it, but it can quietly steal your future wealth.

Brutus unknowingly gave away almost half of what his nest egg could have been—just to fees.

Goldy didn’t fare as badly, but even that 5% sales load cost him over $200,000 over time.

Bucky? He gets to retire with over $1.6 million. He didn't invest more. He just kept more of what was already his.

Wait—Is Hiring an Advisor a Bad Thing?

Not at all!

A great financial advisor can be incredibly valuable—especially when they help you:

Build a strategy

Manage risk

Avoid emotional investing mistakes

Save you from doing something dumb when the market drops 20% 😅

But be selective. If you hire an advisor, look for one who is:

✅ A fiduciary (legally required to act in your best interest)

✅ Fee-only (they don’t earn commissions for recommending products)

✅ Charges a flat fee or hourly rate—not a percentage of your portfolio (don't be like Brutus!)

You can find great advisors at:

Closing Thoughts

If you’re in your 20s or 30s, this message might be the most valuable thing you read all year.

Fees are sneaky. They sound small. They hide in footnotes. They don’t show up as a line item in your account. But they compound—just like your returns.

And just like Brutus learned the hard way… they can cost you nearly $800,000 over a lifetime.

Don’t give your future away. Be like Bucky: Choose low-cost investments, know what you’re paying for, and if you need advice, hire the right kind of help.

Let your money work for you, not for someone else.

– Brett

NextGen Financial Freedom

P.S. Want help analyzing your current fund fees? Drop me a note—I'd be happy to help you figure out how much you're paying and whether it’s worth it.