Middle Class to KickA$$ - Reboot

An updated version of a famous blog post in the FIRE community

Brett Killion

7/26/20235 min read

Have you ever heard of the FIRE Movement? I didn't until a few years ago. FIRE stands for "Financial Independence, Retire Early", and it started to gain traction in personal finance circles in the last 10-15 years. Here is a brief overview of the FIRE movement and its philosophy:

FIRE Movement

The FIRE movement is a lifestyle and financial strategy that aims to achieve financial independence at an early age. It revolves around saving a significant portion of one's income and investing it wisely to accumulate enough wealth to retire early. The core idea of the FIRE movement is to live below your means and avoid unnecessary expenses, thereby maximizing savings and investment opportunities. By adopting a frugal lifestyle and having a large savings rate, individuals following the FIRE movement aim to achieve financial freedom, where they no longer rely on traditional employment for income. While it requires discipline and planning, the FIRE movement offers the possibility of early retirement and the freedom to pursue one's passions and interests on one's own terms.

Influential Blog Post in the FIRE Community

Within the last few months, I recently discovered a podcast called ChooseFI (Choose Financial Independence) where the two hosts interview others who have either achieved financial independence or are on the path to doing so. At the end of most of their podcasts, they ask their guest the same set of questions, including this one: "What is your favorite blog post of all time?" As I listened to more and more episodes, one blog post was mentioned frequently. It was written by a man who calls himself Mr. Money Mustache, and he is famous in the FIRE community for his writings on frugality. The name of the blog post is How to Go From Middle-Class to Kickass. He wrote the article back in 2012 and it made a major impact on those interested in pursuing financial freedom.

I've read it a few times and can relate to what he is saying. His main point in the article is that one variable can make all the difference in the world between working until you are 65 and being able to retire early: your spending rate. He uses a table to compare two hypothetical high-middle-class income families of four and their typical monthly spending. He calls his comparison the "Typical Fancy Professional Worker versus a Future Early Retiree". At the bottom of the table, he shows that the Typical Fancy Professional Worker only saves about 15% of their annual income and (based on his calculations) is 43 years away from retirement based on their lifestyle. However, the frugal Future Early Retiree saves a whopping 74% of their income and can retire in only 7.5 years. Wow!

Reboot Needed

Although this article is "famous" in the FIRE community and makes an incredibly important point in achieving financial freedom, I think it needs a reboot. Here's why:

It was written over 10 years ago and prices/costs have changed since then

He uses high-middle-class income couples in his examples with after-tax annual incomes of $140,000 rather than a more modest income level

He comes from an ultra-frugal mindset (minimalist lifestyle) that turns some people off due to being too extreme. One example: he argues you should live close to your workplace and bike vs. owning a second car

I'm not the biggest fan of how he calculates the "Years to Retirement" part of his comparison, although I understand his logic (you can read how he calculates this in another one of his blog posts The Shockingly Simple Math Behind Early Retirement)

The Reboot

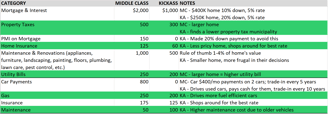

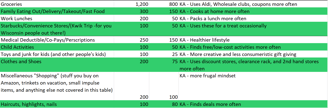

Due to the reasons above, I created my own comparison table of "Middle Class to Kickass" based on the following assumptions:

The comparison is between two families of four in Wisconsin

The parents are in their mid-30's and each one makes $80,000/year ($120,000 after tax)

Both children are in elementary school, so daycare costs are excluded from the comparison

Of each family's annual savings, half goes into their savings account (for short-term savings goals and their emergency fund) while the other half is invested for the long-term

Estimated Investment Annual Return = 7%

Entry-Level Middle-Class Lifestyle

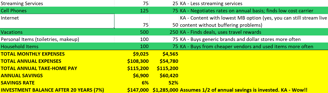

Maybe there's a line item or two that you disagree with or think I'm way off on, but I'm pretty sure I'm in the ballpark with the numbers above. I also think the "Kickass" lifestyle is not a lifestyle of deprivation or severe frugality. NGFF does not believe in saving all your money now without having any fun and waiting until retirement to enjoy your passions. "Entry-Level Middle-Class Lifestyle" is a term I heard on the ChooseFI podcast several times, and that is what you are seeing in the "Kickass" column above. No, the savings numbers are not as impressive as the original How to Go From Middle-Class to Kickass article written by Mr. Money Mustache. He quotes a 74% savings rate for the "Kickass" family in his example. However, I think the 52% savings rate you see above is more attainable and realistic...if you are content with the entry-level middle-class lifestyle.

$1,285,000 in 20-Years?? No Way!

Ummm, yes way!! I would even argue this number is a little conservative and could be way more! How? I'm not even factoring in these assumptions:

The investment growth doesn't include any 401k employer match contributions

The example above doesn't include either spouse earning a pay raise or increasing their income over the next 20 years

The example above assumes the "Kickass" family invests half of their annual savings ($30,210) and puts the other half in their savings for short-term goals. If it was more like a 75/25 split ($45,315 in investing and $15,105 in savings), the investment balance 20 years later would be way more

Closing Thoughts

Mr. Money Mustache is a fixture in the FIRE movement, and his original blog post from over 10 years ago has inspired many people to pursue a life of frugality in order to achieve financial freedom quickly. As much as I like his original post, I thought it needed a reboot. Maybe my example above doesn't get this "Kickass" family to early retirement in 7.5 years like the example from Mr. Money Mustache, but I hope it inspires you to think about pursuing an entry-level, middle-class lifestyle to achieve financial freedom much faster than the typical middle-class family.

What are your thoughts on this? I'd love to hear them. Feel free to contact us for your feedback on this post or any other of our blog posts.