I have a quick challenge for you. In a moment, stop reading this blog (don't worry, I won't be offended) and do the following:

Step 1: Open another browser window

Step 2: Google "best personal finance books"

Step 3: Click on the first 3-5 results and see if the book The Millionaire Next Door appears on the list of recommended books

Ok, ready? Go ahead, and I'll see you back here in a few minutes.

Done already? That was fast! I'm not sure what you found, but I bet I can guess. I'm guessing that every site you looked at had The Millionaire Next Door" listed as one of the best personal finance books. The author of this book, Thomas J. Stanley, interviewed over 500 millionaires and surveyed over 11,000 high-net-worth households. What he found was the characteristics and money habits of how these individuals built their wealth. The focus of this blog post is what Thomas J. Stanley says is the biggest detriment for households to build wealth over time.

Home & Neighborhood

In one of Stanley's follow-up books, Stop Acting Rich, he uses this quote: "The greatest detriment to building wealth is our home/neighborhood environment." He adds, "Most of the self-made millionaires I have studied . . . were able to build wealth precisely because they never lived in a home or neighborhood environment where their domestic overhead made it difficult for them to build wealth." There is actually a triple whammy to your ability to build wealth when you purchase a home at the very top of your budget.

Whammy #1 - The Initial Purchase Price

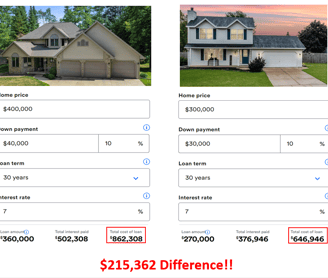

This first one is pretty obvious. If you purchase a $400,000 home vs. a $300,000 home, that's an extra $100,000!! Actually, for most of us, it's more than $100,000...much more! The most common way people finance a home is through a 30-year fixed mortgage. When you factor in interest payments over 30 years, that more expensive purchase price is costing you more than you think.

Take a look at the example below. I screenshotted 2 homes from Realtor.com in the Green Bay, WI area that are currently for sale. The one on the left has a list price of $399,000 and the one on the right is listed at $300,000. Assuming a 30-year fixed-rate mortgage with the current national average interest rate of 7%, take a look at the eye-popping numbers below:

Wow! Imagine what you could do in your life with an extra $215,000.

(Sidebar - It's also kind of depressing to see how much you actually paid for that $400,000 if you make the monthly mortgage payments for the next 30 years: $40,000 down payment + $862,308 loan payments = $902,308...ouch!)

Whammy #2 - Ongoing Operating Costs

This next one is not as obvious. When you buy a more expensive home, you are most likely going to pay higher property taxes. Here are the estimated property taxes for the homes above (both are in Green Bay):

(Note: Property taxes are assumed to remain unchanged in the example above for simplicity.)

In addition, you will most likely incur a higher homeowner's insurance rate due to owning a more expensive property. Throw in higher utility bills for owning a bigger home, and your ongoing operating costs cost you thousands over the long term.

Whammy #3 - Keeping Up With The Jones

This last one is much more subtle. In his book, Stop Acting Rich, Stanley says the following: ". . . the true cost of living in certain homes and neighborhoods is unseen but truly devastating. . . .If you live in a pricey home and neighborhood, you will act and buy like your neighbors...act and be like those around (you)...the more affluent the neighborhood, the more its residents spend...From cars to haircuts, and from wine to watches, those who live in ‘prestige estates’ spend more."

This makes sense. If you are surrounded by neighbors who are buying new, more expensive __________ (fill-in-the-blank: cars, golf clubs, furniture), telling you stories about their most recent expensive vacation, or inviting you out to pricy restaurants, you are more likely to increase your own spending according to financial psychologists.

Our Best Financial Move

A few months before I met my wife, she purchased a small house...a VERY small house (600 square feet - no that is not a typo). Even though it was the smallest house in the neighborhood, it was a well-kept home in a historic Green Bay neighborhood with great neighbors and a park a block away. After we were married, I moved into that house and we lived there for the first eight years of our marriage. After being blessed with our daughter we FINALLY upgraded to a larger, yet modest house, after she turned 1 year old. So yes, all three of us lived in that small house for a year, including our 50-pound dog. (See below...the 2 trees were cut down after we moved out)

Living in that incredibly affordable house early in our marriage became the best financial move we've made. It gave us the freedom for my wife to stay home with our daughter these past several years without cramping our lifestyle. We were not subjected to the triple whammy mentioned above, and it set us up for a more flexible financial future.

Closing Thoughts

If you are considering buying a home, whether you are a first-time homebuyer or looking to upgrade, think about the information above very carefully. Ramit Sethi, the author of I Will Teach You To Be Rich, talks about "lifestyle creep". He states "There are certain spending areas where, once you spend, it's very hard to go back", and he mentions buying a bigger home first on his list.

Hey, it's your life! If it is incredibly important to you to buy a pricy home in a very nice neighborhood, then that's your call. Just keep in mind the more money you commit to your housing, the less financial flexibility you will have to pursue your other goals, passions, and dreams. One of my new favorite podcasts Afford Anything, has a pretty simple philosophy: You can afford anything but not everything.

"The key to wealth building is to live in a home that one can easily afford," according to Thomas Stanley's daughter Sarah Stanley Fallow who has also studied millionaires. So that begs the question: What does "easily afford" mean?

For the answer to that question, stay tuned for NextGenFinancial Freedom's next blog post. Stay tuned!