Where did we leave off? Oh yes, now I remember! Here is the closing thought from NGFF's previous blog post, The Biggest Detriment to Building Wealth:

"The key to wealth building is to live in a home that one can easily afford," according to Thomas Stanley's daughter Sarah Stanley Fallow who has also studied millionaires. So that begs the question: What does "easily afford" mean?

The focus of this blog post is to help answer that question. This is a pretty darn important question to answer. The biggest line item in most people's budget is housing. If you are able to wisely control your spending on this one necessity, it can set you up for great financial flexibility in other areas of your life. Living in a home you can "easily afford" can give you the freedom to invest more money in your passions, have a stay-at-home parent for your children, or retire much earlier than the median retirement age of 64.

What you will see below are different ways to determine your housing budget. Some of these methods NGFF does NOT recommend while others are endorsed by NGFF. I'll use a fictitious couple to highlight the financials behind each budgeting strategy. I will also use real houses currently for sale on the market as of the time of this writing.

Since I live in Wisconsin, we will use Wisconsin homes in the examples that follow. Currently, the median sales price of a home in Wisconsin is $304,000. Home prices can vary greatly within Wisconsin depending on where they are located. Therefore, I chose to use homes located in Jefferson County because the median sales price of homes in Jefferson County is $300,000, close to the median for Wisconsin.

Meet Our Couple

This is Michael and Emily. They are married and both 27 years old with no children. They have been living in a 1-bedroom apartment for the past two years and now are ready to purchase a house. Both Michael and Emily are college graduates and each one earns a salary of $60,000/year. They have excellent credit (both have credit scores over 760) and have saved some money for a down payment on a home. Each one has a car payment of $400/month and student loan payments of $200/month, making their total monthly installment loan payments $1,200.

Let's start with 2 common budgeting methods NGFF does NOT recommend for Michael and Emily.

My Budget is The Maximum I'm Prequalified For

Please, for the love of God, don't do this!! But let's back up for a second.

Being prequalified for a mortgage loan means that a lender has reviewed your financial information and has determined that you have the potential to be approved for a loan. It is the first step in the mortgage application process. To be prequalified, you need to provide the lender with details about your income, assets, and debts. The lender will then evaluate this information and calculate an estimate of how much they may be willing to lend you.

I remember when I was a 27-year-old high school teacher making a whopping $35,000/year, I was thinking of buying a condo. I went to my bank to get prequalified for a mortgage loan and determine how much of a condo I could afford. After they ran the numbers, my bank prequalified me for a mortgage of up to $180,000. I was shocked by this number! I remember saying to myself, "I can afford a $180,000 condo on my salary? Really? Well, I guess I can because that's what the bank said I can afford. They're the experts, so....ok!" (Luckily, I never purchased a condo).

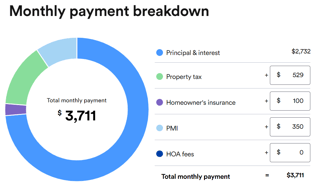

Assume Michael and Emily use this method to determine how much of a house they can afford. Running the numbers on NerdWallet's Mortgage Pre-Qualification Calculator, they could qualify for a mortgage as high as $435,000. They plan to make a down payment of 6% which is the national average down payment percentage for first-time homebuyers. This means they are looking for a home within a budget of $461,000.

Michael and Emily search for homes around this price point in Jefferson County and found this home to buy with a list price of $459,900:

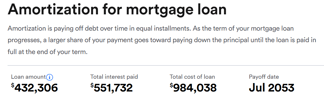

Taking out a 30-year mortgage at a 6.5% interest rate, here are the estimated financials for Michael and Emily for their home purchase using Bankrate's Mortgage Calculator:

The payments on that home cost Michael and Emily over $1 million!!! ($984,038 total cost of loan + $26,100 down payment).

Michael & Emily, listen to me...don't do this!! Yes, it's tempting to purchase the largest house the bank says you can afford. However, as a young couple, your $3,711 monthly mortgage payment will severely limit your financial flexibility, and it's very hard to go back once you purchase a more expensive home like this. There's a reason why there's the phrase "starter home".

The 28% Rule

This is the most common home purchase budgeting rule. If you Google phrases like "how much house can I afford", "how much should my mortgage be", or "what should my monthly mortgage be", you will see the 28% rule all over the place in your search results.

The rule is pretty straightforward: Your monthly mortgage payment should be less than 28% of your monthly gross income.

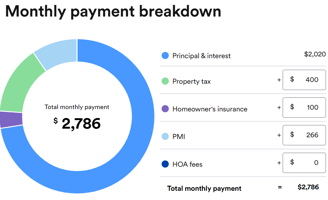

If Michael and Emily follow this rule, their maximum monthly mortgage payment should be $2,800.

Michael and Emily search for homes around this price point in Jefferson County and found this home to buy with a list price of $339,300:

Taking out a 30-year mortgage at a 6.5% interest rate, here are the estimated financials for Michael and Emily for their home purchase using Bankrate's Mortgage Calculator:

This seems reasonable. That's a pretty nice new-build starter home. The 28% rule is the most common rule of thumb when setting a budget for purchasing a home. So you might be asking yourself, "Why does NGFF not recommend this method?".

There are a few reasons:

1) Going back to the quote at the beginning of this article, I want to focus on this one word in bold - "The key to wealth building is to live in a home that one can EASILY afford,". Yes, the 28% rule is the normal rule of thumb, but do you want to be normal? Stealing a phrase from Dave Ramsey, "Normal is broke" in this country. At NGFF, we advocate for you to be different and apply money management techniques to live an extraordinary life, not an ordinary life.

2) The focus of NGFF is personal finance for young adults. Young adults have a HUGE advantage over us older adults...time!! By having extra money beyond basic living expenses, young adults can use those funds for other short-term goals, long-term investing, and more flexibility (leaving a job they do not like, affording to have a stay-at-home parent).

3) Who the heck came up with 28% in the first place?!?! There has to be someplace where it started, but I haven't been able to find it. Why not 30%? Why not 27%?

Michael and Emily, I know what you're thinking, "You're expecting us to buy a crappy house in a crappy neighborhood!"

No, just give me a chance here. Below are two budgeting guidelines to follow that NGFF endorses. Let's see if we can find Michael and Emily a home they would like that they can also easily afford, keeping in mind, a) this is their starter home and b) they can upgrade sometime in the future after their incomes rise and they build their savings.

Here are 2 budgeting methods NGFF endorses both for Michael and Emily...and you!

2.5X Household Income

Simple math on this one: Take your household income and multiply it by 2.5. This is the maximum amount of a mortgage you should take.

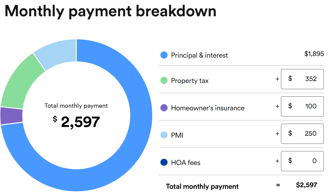

If Michael and Emily follow this method, they can "afford" to take out a mortgage of $300,000 ($120,000 household income X 2.5). The final home price is then determined by how much of a down payment Michael and Emily make. We've been using a 6% down payment in all of these examples because that is the national average. However, if Michael and Emily have enough savings to make a 10% or a 20% down payment, they can then afford $333,000 or $375,000 house, respectively.

Again, let's use a 6% down payment for consistency which makes Michael and Emily's maximum budget $319,000 using this method. They search for homes in Jefferson County and found this home to buy with a list price of $319,000 (actually, the house below was listed at $325,000 but this was the closest price I could find to $319,000 in Jefferson County at the time of this writing):

Michael & Emily Future Home?

Taking out a 30-year mortgage at a 6.5% interest rate, here are the estimated financials for Michael and Emily for their home purchase using Bankrate's Mortgage Calculator:

This might not seem like a huge difference between this method and the 28% Rule, but paying almost $200/month less adds up. Additionally, if interest rates are lower, there is a much bigger gap in monthly payments between this method and the 28% Rule.

The 28% Rule...With A Catch

Wait a second, we're back to the 28% Rule? Yes, but with a catch. This is NGFF's favorite guideline to follow when determining how much house you can afford. Remember, the conventional 28% Rule says no more than 28% of your monthly gross income should go towards your mortgage payment, and it is based on a 30-year mortgage. NGFF's 28% rule is based on a 15-year mortgage.

Well-known consumer advocates like Dave Ramsey and Clark Howard are big fans of the 15-year mortgage, and so am I! Yes, the 15-year mortgage comes with a higher monthly payment than a 30-year mortgage, but not as high as you think. Additionally, a 15-year mortgage typically comes with about a 0.5% lower interest rate which adds up over the long term. Lastly, your can own your home free and clear 15 years earlier and save a boatload of money by not paying your lender interest for another 15 years. You just need to find a more modest home. Do you think we can do this for Michael and Emily? Let's find out!

Remember from the 28% Rule above, their maximum monthly mortgage payment should be $2,800.

Michael and Emily search for homes using this budgeting method in Jefferson County and found this home to buy with a list price of $260,000.

Taking out a 15-year mortgage at a 6% interest rate, here are the estimated financials for Michael and Emily for their home purchase using Bankrate's Mortgage Calculator:

If Michael and Emily make this one very important decision and follow the 15-Year Mortgage 28% Rule, this changes their entire financial future! They are mortgage debt-free by 43 years old and have paid a boatload less interest than any of the other methods mentioned above. Imagine the freedom you could have in your life by not having a huge mortgage payment by your early 40s!!

Side Note: Why does everyone do a 30-year mortgage? Who came up with this number in the first place? Why not a 20-year? Why not a 40-year? Ask your parents, friend, or coworker, and I bet you they took out a 30-year mortgage when they purchased their first house. Then ask them why, and I bet you they will say something like, "That's what everyone does". Don't be like everyone!

Disclaimers

1) In the examples above, I used 6% as the down payment. I'd strongly encourage you to try to save 20% for a down payment to avoid PMI which adds to your monthly payment. For brevity purposes, you can read more about PMI here.

2) With the two budgeting methods NGFF endorses above, I'd rather refer to them as "guidelines" vs. "rules". Every homebuyer's situation is different, and we should not be too rigid when it comes to our recommended budget. If a home that you love will cost you $100 more/month than the guidelines above, go for it! We don't have to live life strictly by our super cool Excel spreadsheets.

3) Home prices vary greatly in Wisconsin and more so in the United States. Homes in cities like Green Bay, La Crosse, and Wausau will be much more reasonable than the examples above in Jefferson County. On the flip side, homes in cities like Madison and Waukesha will be more expensive.

4) All the examples above assume Michael and Emily live in the same home for the entire length of the mortgage. This is often not the case in real life, but the assumption is used for simplicity.

Recap

Before we're done, let's look at the 4 options again for Michael and Emily:

Option #1: Budget = Maximum they are prequalified for (NOT RECOMMENDED...AT ALL!!)

Purchase Price = $460,000

Total Interest Paid = $551,732

Total Cost of Home = $1,010,138

Option #2: Budget = 28% Rule (NOT RECOMMENDED...do you want to be normal?)

Purchase Price = $340,000

Total Interest Paid = $407,699

Total Cost of Home = $747,699

Option #3: Budget = 2.5X Household Income (RECOMMENDED GUIDELINE)

Purchase Price = $319,000

Total Interest Paid = $382,693

Total Cost of Home = $701,553

Option #4: Budget = 28% Rule, 15-Year Mortgage (FAVORITE GUIDELINE)

Purchase Price = $260,000

Total Interest Paid = $126,872

Total Cost of Home = $386,872

Closing Thought

According to Sarah Stanley Fallow and her father Thomas Stanley (the author of The Millionaire Next Door), the key to building wealth is to live in a home that one can easily afford. When you are in the market for your first (or next) home, keep the 2.5X Household Income and 28%, 15-Year Mortgage guidelines in mind. If you do, your future neighbors just might be living next to you...the millionaire next door!