Pay Yourself First: A Life-Changing Concept

Learn what "pay yourself first" means and how you can apply it to change your financial situation...forever!

"PAY YOURSELF FIRST!!" (sorry, I don't mean to shout) - I'm not exactly sure when I first heard this phrase. I'm not exactly sure where I first heard this phrase. But being introduced to it in my early adulthood changed my thinking on personal finance forever. I think this phrase is so important that I put it as a short answer question on the final exam for the personal finance course I teach at Lakeland University. And, the underlying concept behind it is so simple. Do you like simple? I do! Do you want to change the trajectory of your money management? Of course, you do! (otherwise, you wouldn't be reading this blog on a personal finance website). So let's dig in!

WHAT DOES "PAY YOURSELF FIRST" MEAN?

NextGen Financial Freedom's Definition - Whenever you receive income (usually from a paycheck), you put a portion of that income into your savings/retirement accounts first before paying your bills or any other spending

Like I said...simple! At the same time, it's the opposite of what many of us learned growing up. At a young age, I thought savings worked like this:

Receive a paycheck

Spend (necessities & discretionary)

Save (whatever's left over...IF there's anything left over!)

Let's make a simple tweak to the steps above. Just flip-flop Steps 2 & 3.

Receive a paycheck

Save

Spend (whatever's left over)

Tada!! That's the "pay yourself first" concept!

DIGGING A LITTLE DEEPER

Throughout my financial education journey, I try to learn money management skills and philosophies from several different sources. Two of my favorites are Dave Ramsey and Ramit Sethi. I show many Dave Ramsey videos in the personal finance course I teach at Lakeland University and Ramit Sethi's book, I Will Teach You to Be Rich is a required reading in the course. Although they have different philosophies and disagree on several topics, they both agree that our money psychology and behavior are way more important than our financial knowledge. When you apply the "pay yourself first" technique to your own finances, you are using money psychology and behavior to your advantage.

How? Well, if you like math, maybe you can relate to these two equations:

Income - Expenses = Savings

Income - Savings = Expenses

Both equations are mathematically the same but notice the difference between the two. The first equation prioritizes expenses. People following this mentality are basically saying, "I'll save any money from my paycheck that is left over after paying all my bills and other 'stuff'". That's the mentality of many Americans living paycheck-to-paycheck. If you read my first blog post, 73% of millennials live paycheck to paycheck according to a recent LendingClub survey. I'm guessing most of the 73% try to save money using this formula but never get ahead.

The second equation prioritizes savings. People following the "pay yourself first" concept are basically saying, "I'm going to prioritize my savings/retirement/other goal-based funds and then spend whatever is left over." That's money behavior and psychology that works in your favor! In essence, using this technique you are doing two important things at the same time: 1) building your savings and 2) limiting your spending.

It's kind of like giving yourself a small pay cut. Assume your bi-weekly paycheck is $1,500. Suppose you decide to pay yourself first $100 each paycheck and you put that $100 into your savings account immediately. Now, you are free to use the remaining $1,400 for your living expenses and discretionary spending.

I'm using round numbers in that example, but here's another way to think about it. The Automatic Millionaire by David Bach is another book that is required reading in my college-level personal finance course. He devotes an entire chapter to the "pay yourself first" concept and gives this guideline: pay yourself first one hour a day of your income. Suppose you work 8 hours/day and you get paid $25/hour. Bach recommends you "pay yourself first" $25 for that day's work. For a bi-weekly pay period, that comes out to $250 you are saving for your future self. Not a bad way to think about it, huh?

Ok, ok, I know you have questions. How can I remind myself to put money into savings immediately after getting paid? Where should I put my savings? How can I even do this when I'm struggling just to pay for everything as it is? You sound like my students! These are all good questions, so I'll do my best to answer them.

AUTOMATE YOUR SAVINGS

Pay yourself first...AUTOMATICALLY!!! (darn, am I shouting again?) - This is the key to the "pay yourself first" concept. You will not succeed and be able to follow this plan unless you automate your savings. Both you and I know that we are not disciplined enough to remind ourselves to manually transfer money over to our savings or investment accounts. We're busy people! I don't know about you, but I don't have the discipline to remember to do this anytime I get paid.

The technique of automating your savings is so important, David Bach devotes another entire chapter to automating your savings in The Automatic Millionaire (it's in the darn title of the book for crying out loud) and Ramit Sethi lists "Automating Your Finances" as one of his 7 Big Wins of Personal Finance. So how can you automate your savings? There are two main ways:

Payroll Deductions - Using the direct deposit form from your employer, set up a system that directs funds to your savings/investment accounts. (Example: Your employer automatically sends a percentage of your paycheck to your 401(k))

Scheduled Checking Account Transfers - Set up scheduled transfers from your checking account to your savings/investment accounts that happen automatically on specific dates

Paying yourself first automatically takes the discipline factor out of the equation. Most of the time your savings is being built behind the scenes without you even realizing it! These automatic transfers are happening whether you are working, sleeping, on vacation, or just doing "life". I like how Brad Kolntz, certified financial planner and financial psychologist, states it in this article, "Automation is one of the most powerful financial hacks available to us."

Here's a true story from just a few months ago. I received a text from my wife that said, "Hey Honey, $XXX was taken from our checking on 2/22 for what I think is our Roth. Is this right? Can you check on this please?" I checked on it, and sure enough, that money was taken out of our checking account automatically and went into our Roth IRA retirement accounts. See, we even forgot what day of the month we had our automated transfers! I have no idea what we were doing at the moment the transfer hit, but we didn't have to remind ourselves to make it happen. One last time, automating your savings is the key to "paying yourself first".

WHERE SHOULD I PUT MY "PAY YOURSELF FIRST" MONEY?

There are two main time horizons to save for your future self: 1) short-term and 2) long-term. Below are some options/suggestions of where you should put your savings for each one.

SHORT-TERM SAVINGS

Basic Savings Account - Use the savings account at the institution you already have at your current bank or credit union. In my opinion, this isn't the best option, but it's the easiest to get started with.

Online Savings Account - This is my favorite option! Federally insured online savings accounts are just as safe as your bank's savings account. The biggest benefit of an online savings account is the interest you earn. Oftentimes, you can earn 10X as much interest as your current bank's savings account. As of writing this blog, the national average interest rate on a basic savings account is 0.42%. As of July 2023, the best online savings accounts offer interest rates between 4-5%.

LONG-TERM SAVINGS

***Note: I won't get into too much detail in this post on the two main options below. Let's keep it simple for now and save the details for a later blog post.***

Employer's 401(k) - Especially if your employer matches up to a certain percent of your salary. Hey, that's free money they're giving you! Not to mention the tax deduction you get when you contribute to this type of retirement account.

Roth IRA - This type of retirement account comes with several advantages. The biggest advantage is that any earnings in this account (stock & bond price appreciation, dividends, interest, etc.) grow TAX FREE!! That's right, you do not get taxed on any money you withdraw from this account after age 59 1/2.

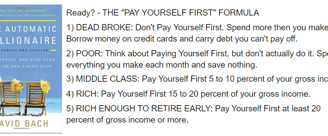

HOW MUCH SHOULD I PAY MYSELF FIRST?

Good question! This depends on where you are currently in your financial situation. As mentioned above, David Bach in his book The Automatic Millionaire gives a general guideline of paying yourself one hour a day of your income. However, I like the "Pay Yourself First" formula he outlines in a different part of the book:

I don't know about you, but I'd rather be in one of the last two categories.

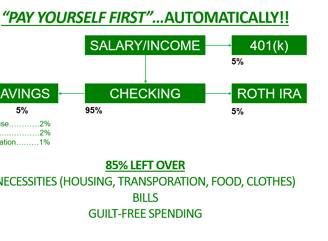

VISUAL AID

For those of you who are more visual learners, below is a diagram I shared during my virtual webinar discussion with the First Generation Professionals of Milwaukee organization:

For simplicity reasons, taxes are ignored in the diagram above. Also, I'm not saying a 5%, 5%, 5% allocation between savings, your 401(k), and your Roth IRA is best breakdown. Rather, I'm just using round numbers for illustration purposes.

I CAN'T DO THIS! I DON'T HAVE ENOUGH TO SAVE

Oh my gosh! Here we go with the excuses.

"I don't make enough money to do this."

"I'm barely getting by just paying my bills."

"This is great in theory, but not for my financial situation."

When I listen to podcasts on topics such as money management, investing, and starting a side hustle, I keep hearing the same advice over and over again: the biggest step you can ever take is...getting started! (Nike's slogan: Just Do It) I like Clark Howard's advice on starting small and gradually increasing your automatic savings over time. Start by setting up an automatic transfer of just $10 from your checking to your savings account after every paycheck. Then, after a while when you realize that wasn't so bad, bump it up to $20/paycheck. Then $30/paycheck, and so on. This "baby steps" approach is less daunting and gets you moving in the right direction.

CLOSING THOUGHTS

According to Credit.com, the median savings account balance for individuals under 35 is $3,240. The methods most of us are using to save money are not working. Every personal finance guru out there has different philosophies on money management, but I bet you they all agree on one thing. Whether it's Dave Ramsey, Clark Howard, Suzy Orman, Ramit Sethi, or NextGen Financial Freedom, they all agree that paying yourself first AUTOMATICALLY needs to be a top priority in your money management system.

Feel free to reach out to NextGen Financial Freedom for any comments on this topic.